There is a lot of debate in the media about the pros and cons of private health insurance. People are often asking, “Should I get private health cover?”

Opinions about private health cover are changing. Saving money when it comes to tax time is an important part of the decision.

According to Australian consumer watchdog, Choice, cheaper private health policies that are used to be exempt from paying the Medicare Levy Surcharge at tax time are often criticised because those cheap plans cover minimal treatments – leaving customers out of pocket for health services they might need.

With cheaper health cover plans, you gain the benefit of avoiding extra taxes and surcharges, but you could have less coverage for treatments than you might need.

More than half of the Australian population – about 13.6 million people – have private health insurance, many of whom don’t fully understand what they are getting for their money and what they are covered for but they choose to have cover for several reasons.

Responding to growing consumer debate, the Australian Competition and Consumer Commission (ACCC) has called for standardisation of policies across providers.

In response, the Government have recently made changes to private health insurance to make it simpler and easier for consumers to choose the cover that best suits the needs of the general public.

The first wave of reforms included the introduction of four easy to understand tiers, discounts for young people, improved access to mental health treatment, and higher excesses in exchange for lower premiums.

Why is Etax writing about health cover?

There are many arguments for and against private health cover. But the one thing most people can agree on is, paying for private hospital cover can save Australians tax money.

That’s because the Australian Government designed a system that uses tax to ‘encourage’ everyone to get private cover, even though we have a national healthcare system – Medicare. If you don’t have private cover, then as your income grows over time, the amount you pay to the Government in extra taxes increases so much, that getting private cover can become cheaper than paying that tax surcharge.

But choosing the right plan at the right cost is not simple. A cheap plan or an expensive one? Hospital or extras, or both? Which insurers are better? What will be covered?

Private health cover is something many Etax clients ask about, so let’s look at this more closely and find some good resources for making decisions about private cover.

Let’s start with the basics, plus a few common questions:

What is private health cover?

It is an insurance policy you pay for monthly or yearly, and it pays for part of your medical expenses when you need treatments or hospitalisation.

There are two types of private health cover:

- Hospital – to help when you need to go to hospital. This covers you for doctors, treatments, overnights rooms and theatre costs.

- General (usually known as extras) – to help with ancillary treatments such as optical and dental care plus some alternative or allied health services like physio and massage.

Private health policies can be often sold with a mix of hospital and extras cover.

According to Private Health Care Australia, 52% of Australians have private health cover.

Private health cover eases the burden on our public health system.

Private health cover can provide policyholders with extra benefits like;

- the ability to choose the hospital and the date of medical treatments and operations,

- better quality of care with private room options,

- access to special services like private rooms or nicer maternity wards,

- shorter wait times,

- cover for dental and optical expenses,

- a sense of security, should the worst happen,

- a good way to pay less tax. (see below)

Does private cover work?

Yes. For many Australians, private health cover makes sense. The right health insurance policy provides you with peace of mind and security when you need it.

However, a growing reality is that many policyholders, especially those on lower or medium incomes, simply cannot afford the premiums and are dropping out of private cover.

Why are some people quitting their private health cover?

Fifteen per cent of Australians with private health insurance dropped or reduced their cover during the pandemic.

According to a Galaxy poll, another half a million threatened to do the same in the lead up to the annual price increase this April.

Daniel Graham, from Choice, pointed out price increases of 54% in the last decade, while the consumer price index (a measure of inflation) grew only 20%.

News coverage suggests the key reasons for this exodus away from private health is due to:

- The cost. Annual fee increases, far above CPI, move the better quality private health polices beyond the reach of many Australians.

- With many policies, you still pay out of pocket for part of the medical services you need; this “dollar gap” is the difference between the amount charged by a medical specialist or hospital and the lower amount paid by the policy. With expensive plans this gap can be smaller (or in some cases, top plans leave no gap) but with common, cheaper plans the gap looks more like a chasm, leaving some lower-income patients with unexpected bills.

- Confusing policies that are difficult to understand and even harder to compare mean people sometimes don’t get the cover they expected, but don’t realise until it’s too late.

What’s the alternative to private health cover?

Medicare, our public system, looks after all Australians and Australian residents.

Pros

- Quality of care in our public hospitals usually rivals that of private hospitals.

- Public hospitals sometimes have a broader spectrum of equipment and specialists in each location, which means that patients can undergo multiple tests, scans and procedures in one place.

- Many procedures and operations require no out of pocket expenses from the patient.

Cons

- Waiting times can be long. This can be a real issue for people waiting for operations such a knee or hip operations, where quality of life is severely diminished.

- You have no choice when it comes to when or where your treatment, consultations or operations are. If you are unable to make a date sent to you, you may drop to the bottom of the list again.

- Under-funding is evident where some waiting rooms are slow, understaffed, overcrowded. This can commonly result in a 2-4 hour wait.

- Medicare does not cover general care, such as dental treatment or optometry.

The Medicare system is funded by government revenue and via the compulsory Medicare Levy that most Australians pay to the ATO in their taxes. The Medicare Levy currently takes 2% of our annual income.

Higher income earners are ‘encouraged’ to take out private hospital cover in order to ease the burden on the public system, and if they don’t, the levy can cost them a LOT of money.

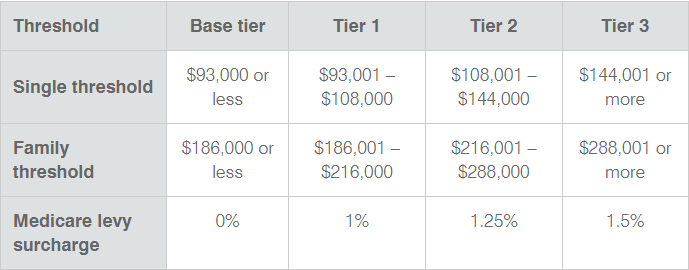

Medicare Levy Surcharge: This is how private health cover can create tax savings

People earning $93,000 or more ($186,000 or above for families) are also required to pay an additional 1-1.5% of their annual income to the government. This is called the Medicare Levy Surcharge.

Medicare Levy Surcharge rates (sourced from the ATO)

* The family income threshold increases by $1,500 for each Medicare levy surcharge dependent child after the first child.

Example: How John’s private health cover saves him money at tax time

John is 29, lives in Queensland and earns $110,000 a year. John’s income puts him over the $93,000 threshold so, without private hospital cover, he’ll pay 1.25% of his taxable income to the Medicare Levy Surcharge (MLS). This equals $1,375 a year.

Instead John chose a typical QLD private hospital cover plan costing $1,250 for young singles like him. John is also eligible for the Australian Government Private Health Insurance Rebate (8.93% of his hospital cover). Because John has private hospital cover, he does not have to pay the Medicare Levy Surcharge.

- Without hospital cover, John will pay the Medicare Levy Surcharge at $1,375 per year

- With basic hospital cover, John pays $1,138 after the Private Health Rebate

- With hospital cover, John’s annual tax saving is about $237

(NOTE: Only private hospital cover creates an exemption from the Medicare Levy Surcharge. Extras does not affect your tax situation, so that cost is all paid by you. The average cost for hospital plus extras cover in QLD $1,831. See below for average costs across Australia.)

Lifetime Health Cover is a financial loading payable on top of your policy if you fail to take out (or keep) Private Hospital cover before your 31st birthday. This amounts to 2% of the policy cost PER year for EVERY year you are over 30, up to a maximum of 70%.

One big question for Australians:

If private health cover won’t take care of my common medical needs, is it better than paying into a public medical system that does?”

Our conclusion

You simply need to do the sums (or ask a tax agent for help), think about what you can afford, think about how much you value the benefits of private health over public, and make a decision that fits you best.

If you make a good income

Plus you can afford a high-level private plan with minimal gap costs and you value good benefits, services and a sense of security, then a comprehensive private plan probably makes sense for you. But as a higher income earner, you probably won’t see a tax advantage (and Federal Government rumours suggest that private health tax advantages might disappear completely for higher income earners).

If you make a lower or average income

When you do the sums, a private hospital plan means a bigger tax refund for you, and if your private cover won’t change your own decisions and spending to leave you out of pocket, then “yes” to private cover might be a “no-brainer”.

On the other hand, if you buy basic private hospital cover just to avoid paying a bit of tax, but end up using lots of expensive health services and pay an out-of-pocket gap each time, that might put you behind financially.

This does not mean that you should ignore private health cover. It simply means that IF you choose the private health cover option, it makes far more sense to purchase a policy that actually looks after you when you need it.

The decision about whether to get private health can be complicated, so you need to decide how important each of these things are to you personally:

- The financial costs

- The tax benefits

- Access to private facilities and services

- Better care in emergencies (if you have the right plan)

- Access to better services if you need maternity or other special services

- And how much you value (and will actually use) extras if you decide to pay for them…

…that’s a lot for each person to consider.

Try some of the links from Choice and the Guardian down below – they have useful interactive tools that help you decide whether private health makes sense for you.

So what should I do?

When choosing your private health cover option, we suggest it’s a good idea to take your time. Concentrate on getting yourself and your family an affordable policy that provides everything that you need (and not including items you don’t need, eg. retirees don’t need maternity services).

- Read (lots) so you really understand what you need.

- Talk to friends, family and work colleagues.

- Ask health professionals for advice, where possible.

- Ask private health cover providers plenty of questions and never worry about asking too many. Tell them what you need and also what you don’t want to pay for.

- Use a checklist to make sure you don’t miss anything out when making your decision.

Useful resources

During our research, we came across some great websites to help you make your private health cover decision:

PrivateHealth.gov.au: Health Insurance Explained

Guardian: Interactive health insurance calculator

Choice: Do I Need Health Insurance? (Interactive Quiz)

Choice: Compare Health Policies (a powerful tool, but for Paid Members Only)

Compare Club: Choosing a health fund

PrivateHealth.gov.au: Lifetime Health Cover Loading calculator

Choice: Hospital Cover: What you need to know

Choice: Health Cover Checklist

Choice: Hints and Tips

Canstar: Average costs for health cover